I took some clients for a coffee the other day.

Lovely couple. Successful. Decent. The sort of people you warm to quickly because they’ve clearly worked hard their entire lives, raised a family, built something worthwhile, and carried their responsibilities without making a song and dance about it.

They hadn’t really had to worry too much about money since their children left home seven years ago. The mortgage was under control. The pensions were there. The savings had built up. Life, on the surface at least, looked pretty settled.

We were standing at the counter when the barista smiled and asked the question.

Small, medium, or large?

He didn’t hesitate. He didn’t look out the window. Didn’t stare into the middle distance. The answer was out before she’d finished asking. Three seconds. Maybe less.

And I smiled to myself. Because two hours earlier, sitting in my office, I’d asked them both a remarkably similar question.

What size retirement are you planning for?

That one took a little longer. In fact, it stopped the conversation completely.

I had framed it simply. Nothing complicated. No spreadsheets. No jargon. No clever financial planning language. Just three broad choices.

Small – There is the retirement where the basics are covered. The bills are paid, the heating is on, there is food in the fridge, and life ticks along.

Medium – The retirement with a little more room in it. A holiday or two. A few treats. A meal out without feeling guilty. Some breathing space.

Large – The retirement most people had in mind while they were working hard for all those years. The one with freedom, travel, generosity, family, comfort, and the ability to say yes more often than no.

His wife looked at him as if to say “I think this is your department.”

He went quiet for a while and looked out my window. After a few seconds pause (that actually felt a lot longer), he said something like “well, I suppose the best we can get for what we’ve saved so far” . Not a bad answer. In fact a very human answer, because that is exactly what people say when they haven’t thought about it much but don’t want to admit it!

This man — who knew instantly what size coffee he wanted — had never once stopped to decide what size retirement he was ordering.

And he’s not alone. Not by a long stretch.

I meet people like this all the time. Business owners. Professionals. Senior managers. Couples who have earned well, saved sensibly, built pensions, paid down mortgages, raised families, and assumed that because they have been careful, they are probably going to be okay.

And they may be.

But “probably okay” is a very thin pillow to sleep on when you are about to make one of the biggest financial decisions of your life.

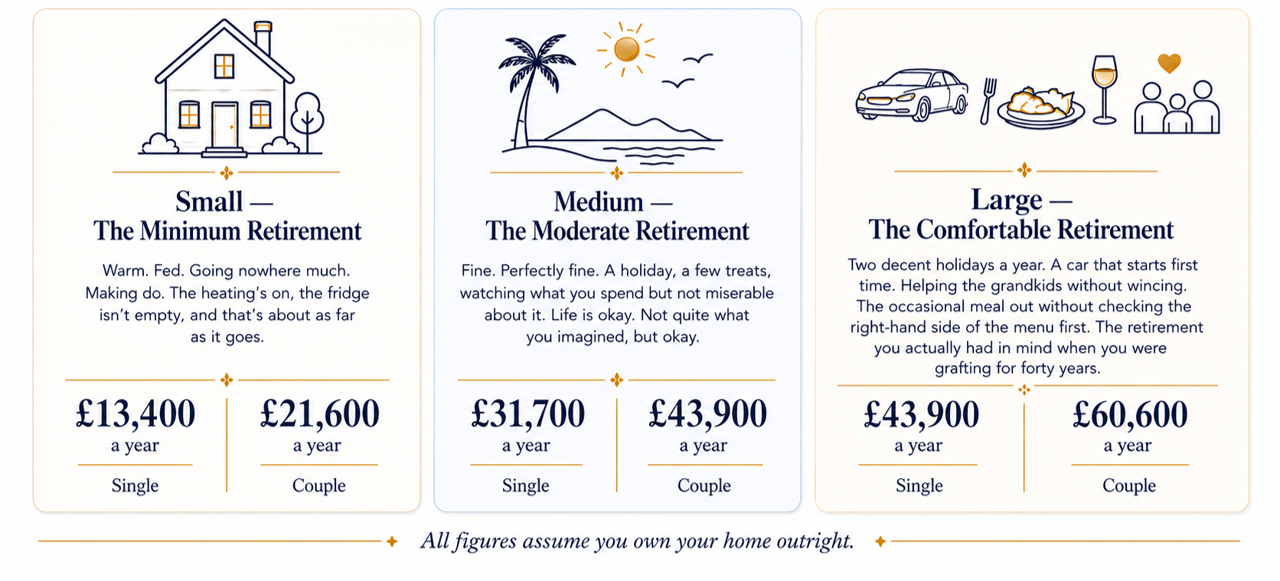

The Three Retirement Living Standards: Minimum, Moderate and Comfortable

The good news is that somebody has done the hard work on this.

The Pensions and Lifetime Savings Association publish what they call the Retirement Living Standards — a properly researched, real-world breakdown of what each kind of retirement actually costs.

In other words, it gives us a menu. Three sizes. Proper numbers. No guessing.

What size retirement do you want? This infographic shows the annual income needed for a minimum, moderate and comfortable retirement, for both singles and couples

What the State Pension Covers — and What It Doesn’t

Now thankfully, the full new State Pension is £12,548 a year. Which means — just about, just barely — the State will order you a small.

But only if you have earned it. To get the full new State Pension, you normally need 35 qualifying years of National Insurance contributions. Fewer years than that, and even the small gets smaller.

And that raises the question most people avoid.

Is Small What You Had in Mind?

Because the moment you decide you want something better — and I suspect you do — the numbers shift dramatically.

A couple aiming for a comfortable retirement need to find an extra £18,804 every year on top of the State Pension. Not once. Not for a few months. Every year, potentially for the rest of their lives.

A couple aiming for large — with both full State Pensions combined sitting at around £25,096 — still faces a shortfall of £35,504 a year.

That’s not a gap. That’s a chasm.

And most people — successful people, busy people, people who’ve done everything right They might have pensions. They might have ISAs. They might have savings. They might even have rental income, a business, or investments they have accumulated over the years. But many still have absolutely no idea whether they’re on course to bridge it. Not because they’re foolish. Because nobody had ever sat down with them and shown them the picture.

And this is the part many people miss – there’s a difference between having money and having a plan for your money. One is a comfort. The other is a strategy.

You can have a pension statement showing a large number and still not know whether you can afford to retire.

You can have investments and still not know how much income they can safely produce.

You can be wealthy on paper and still feel nervous about spending.

You can be careful with money your whole life and still enter retirement without a proper plan.

And here’s something else I’ve learned after years of these conversations — the money gap is not the only part to solve. Sometimes the harder part is everything that sits behind it. The questions people haven’t asked themselves yet. The conversations they’ve been putting off. The assumptions they’ve made and never tested.

The conversations couples have gently avoided because life was busy, work was demanding, and retirement always felt like something that belonged to the future.

- When will you actually stop working?

- Will you stop all at once, or gradually?

- What do you want the first ten years of retirement to look like, while you are still fit, active and able to enjoy it?

- How much do you want to give to your children?

- What rate of return is required on your pension to meet your spending needs?

- What happens to your plan if markets fall at the wrong time?

- How much can you afford to spend each year?

- What happens if one of you lives much longer than the other?

These are not cheerful coffee shop questions. But they are retirement questions. And avoiding them does not make them disappear. It simply means they sit quietly in the background, waiting for a less convenient moment.

How I can help

Firstly, I’ve developed a retirement scorecard. 51 questions covering 10 different retirement challenges you will face. It takes about twelve minutes to complete.

It won’t crunch your pension numbers or tell you exactly how much you need. What it will do is hold a mirror up to your thinking — asking you a series of questions, some financial, some not, that help you work out which size retirement you actually want and how prepared you genuinely are to achieve it.

Most people find it revealing. Not because the questions are complicated. Because they’ve never been asked them before.

It’ll help you work out whether you’re ordering a small, a medium, or a large — and whether your current plans are anywhere near up to the job of delivering it.

Click this and take the scorecard. It costs nothing.

But here’s the honest truth. The scorecard will show you the shape of the problem. It won’t solve it.

Get a Personalised Retirement Cash Flow Plan

Secondly, if you want the actual numbers — the year-by-year picture showing when you can retire, how much you can safely spend, how long your money may last, and whether your current plans are enough — that needs a proper personalised cash flow plan.

That is something I offer for a fixed fee of £595.

Not thousands. Not an open-ended arrangement. Not a vague chat that somehow turns into a sales meeting. A proper planning exercise designed to give you clarity before you make one of the biggest decisions of your life.

For many people, it answers the question they have been carrying quietly for years. “Are we going to be okay?” And that question matters. Because the most dangerous time to discover you have ordered the wrong size retirement is after you have already left the counter.

For most people, that’s the most valuable £595 they’ll ever spend.

The numbers above are the wake-up call. The scorecard is the mirror. The cash flow plan shows you the truth.

And once you can see the truth clearly, you can start making better decisions. Not guesses. Not assumptions. Decisions.

And that is when retirement planning starts to feel less like a leap of faith, and more like a path you can actually walk.

If you are within five to ten years of retirement and want to know whether your pensions, savings and investments are enough, start with the Retirement Readiness Scorecard. It is a simple first step towards understanding whether your current plans are likely to support the retirement lifestyle you want.

Frequently Asked Questions About Retirement Planning

How much does a couple need to retire comfortably in the UK?

A couple aiming for a comfortable retirement may need around £60,600 a year, depending on their lifestyle, housing costs, health, family commitments and travel plans. The key question is not just what the headline figure is, but whether your pensions, savings and investments can support that level of spending for the rest of your life.

How much does a single person need in retirement?

A single person’s retirement income need will depend heavily on whether they own their home, their lifestyle expectations and how much flexibility they want. The Retirement Living Standards are a useful guide, but the real answer comes from building a personalised retirement cash flow plan.

Does the State Pension cover a comfortable retirement?

No. The full new State Pension provides a valuable foundation, but on its own it is unlikely to provide the retirement most people describe as comfortable. For many people, the gap needs to be filled by pensions, ISAs, savings, investments, rental income or other assets.

How do I know if my pension is enough to retire?

You need to understand how much income your pension can realistically provide, how long it may need to last, what investment return is required, what tax you may pay, and what happens if markets fall or your circumstances change. A pension statement gives you a number. A retirement plan shows you what that number can actually do.

What is retirement cash flow planning?

Retirement cash flow planning is a year-by-year forecast showing your income, spending, pensions, savings, investments and tax position throughout retirement. It helps answer practical questions such as when you can retire, how much you can spend, whether your money is likely to last, and what changes may improve your position.

Can I afford to retire at 60?

Possibly. But retiring at 60 usually means funding several years before State Pension age, which can place more pressure on pensions, savings and investments. The only sensible way to answer the question is to model your personal numbers properly.

What should I do first if I am unsure about retirement?

Start by getting clear on the retirement lifestyle you want, then test whether your current pensions, savings and investments are likely to support it. The Retirement Readiness Scorecard is a useful first step, and a personalised cash flow plan gives you the detailed financial picture.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}