It’s that time again.

A new tax year has quietly opened its door, following an Easter break which has hopefully given you a rare moment to pause and reflect on the things that really matter. Because Easter, for many, has a way of doing that. It creates just enough space to step off the treadmill for a moment… to lift your head up from the day-to-day and think a little more clearly about life, faith, family, priorities, and where things are heading.

And it’s often in those quieter moments that allow you to assess whether your finances are organised in the right way and whether you’re making the most of the opportunities available to you. Which is exactly where the new tax year naturally comes into focus.

Because with it comes a fresh set of pension and ISA allowances, a clean slate, and a chance to either reinforce what you’re already doing well… or make a few smart adjustments that could make a meaningful difference over time.

And yet, it’s often at precisely this point—when the opportunity is right in front of you—that a different kind of question that may be creeping in. Not whether you should act… but whether now, with everything that’s going off in the world, is the right time to act?

Now, I know not all of you are in the same position.

Many of you have already done the heavy lifting. You’ve accumulated, you’ve planned, and you’re now drawing from your investments to fund the life you’ve worked hard to create. Some of you are still building your wealth —thinking about topping up ISAs, making pension contributions, or putting surplus cash to work. If I’m honest, this article is aimed mostly at the second group but, for those of you that are fully invested already, I still think this month’s article will be worth reading.

Because whether you’re investing new money or drawing an income, the same uncertainty creeps in. The headlines. The market movements. The sense that maybe—just maybe—timing this right matters more than usual. So regardless of which camp you’re in, the underlying question tends to be the same:

“With everything going on, should I be investing or withdrawing now… or would I be better off waiting?”

And it’s a fair question. In fact, it’s exactly the kind of question that comes up at the start of almost every new tax year.

So, I thought it might be more useful to take a look at exactly what IS going off right now and then provide a different thought process to help you make a decision.

The Backdrop – What’s Actually Going On

Most of you will already be aware that tensions between the US and Iran are currently playing a major role in driving market sentiment. In fact, if you’ve been following the news, you’d be forgiven for thinking Russia and Ukraine have quietly shook hands and made friends.

At its core, the current conflict with Iran and the US is an ideological one. But markets don’t react to ideology – they react to consequences – and in this case, the consequence is energy.

Because when tensions rise in that region, attention quickly turns to one critical spot in the global system: the Strait of Hormuz. It’s a narrow stretch of water, but an incredibly important one, because around a fifth of the world’s oil supply passes through it every single day. Which means even the possibility of disruption is enough to move markets.

Oil prices don’t wait for events to happen—they move on expectation. So as soon as there’s a credible risk to supply, prices tend to rise quickly – and this is where the ripple effect begins.

Higher oil prices don’t just affect energy companies. They feed directly into the real economy. Transport becomes more expensive. Manufacturing costs increase. Supply chains feel the pressure. And before long, those higher costs start working their way through to the prices we all pay for goods and services.

If you want to see how quickly this plays out, you don’t have to look very far.

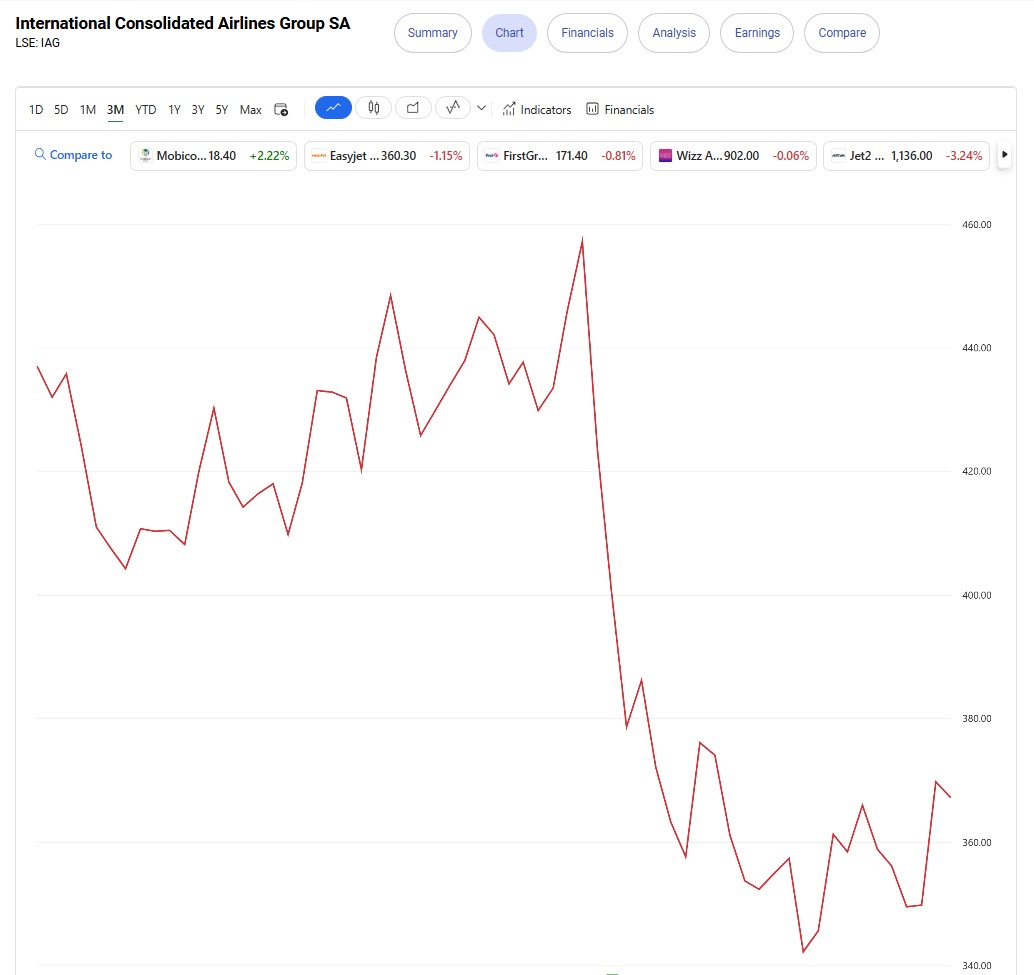

Take International Airlines Group, the owner of British Airways, as a simple example. Fuel is one of the biggest costs for any airline, so when oil prices rise, investors don’t hang around—they immediately reassess future profitability. And that change in expectation shows up in the share price almost instantly.

Take International Airlines Group, the owner of British Airways, as a simple example. Fuel is one of the biggest costs for any airline, so when oil prices rise, investors don’t hang around—they immediately reassess future profitability. And that change in expectation shows up in the share price almost instantly.

Despite no sudden collapse in demand for travel, and no immediate deterioration in the business itself, IAG’s share price has come under pressure over recent months as higher fuel costs and geopolitical risk have been priced in.

What’s important here isn’t the exact numbers—it’s the speed of the reaction.

Nothing fundamental changed overnight. People didn’t suddenly stop flying. The business didn’t break.

What changed… was expectation. And markets move on expectation.

So in a relatively short space of time, an ideological conflict evolves into a geopolitical risk… which centres on a shipping route thousands of miles away… which pushes up oil prices… which impacts corporate profitability… which then feeds directly into stock market valuations.

It doesn’t stop there either.

Transport and logistics companies feel it because fuel is such a major cost. They pass those increases on to manufacturers and retailers. And eventually, those costs land with you and I at the shopping till – which is where it then becomes an inflation story too.

Inflation had been showing signs of easing, but situations like this have the potential to keep it stubbornly higher for longer. And that matters, because it’s exactly what central banks are watching when deciding what to do with interest rates.

So while nothing has fundamentally broken, the environment has shifted—just enough to create uncertainty which, to be honest, that’s not exactly unusual.

But to come back to the main point of this article —the real question isn’t just what’s happening in the world, but what you should do about it, especially because the new tax year has begun and fresh allowances of up to £160,000 are available in pensions and ISA’s.

Because, while we have no control over global events or what markets decide to do in the short term, we do have control over how we respond to them. And in many ways, that response is what ultimately shapes long-term outcomes far more than the events themselves. It’s not about predicting headlines, it’s about deciding how to act in spite of them. And this is exactly where different perspectives can be helpful.

Around the Table – Different Ways to Look at the Same Situation

Imagine, for a moment, that instead of just making your own mind up of whether to invest today or not, you were able to quietly step into a room where these types of investment conversations are actually happening.

You’re not part of the discussion—you’re simply observing like a fly on the wall—listening to how experienced investors, economists, fund managers and analysts are debating what all of this means and, more importantly, what they would do next.

So, let’s step into the room together, take a seat, and lets listen and observe.

Around the table are five or six people, all intelligent, all experienced, all looking at the same set of facts—but each interpreting them through a slightly different lens. And as you listen, it’s worth asking yourself a simple question: Which one of these experts sounds most like you?

Cautious Colin is usually the first to speak—measured, analytical, perhaps slightly conservative in his tone. He’ll point out, quite reasonably, that situations like this can escalate even further, that markets don’t respond well to prolonged uncertainty, and that we could see further volatility and downside if things worsen. It’s a sensible view, grounded in risk awareness, although it doesn’t necessarily make you feel any more comfortable.

Then you have Gary Growth, the long-term investor, who tends to take a step back and look at the bigger picture—calm, confident, and comfortable with a degree of uncertainty. His view is that markets have been through wars, recessions, crises and shocks many times before, and despite all of that, they’ve continued to move forward over time.

Then you have Gary Growth, the long-term investor, who tends to take a step back and look at the bigger picture—calm, confident, and comfortable with a degree of uncertainty. His view is that markets have been through wars, recessions, crises and shocks many times before, and despite all of that, they’ve continued to move forward over time.

From his perspective, periods like this, where uncertainty pushes prices down or creates volatility, are often where opportunities begin to appear. He would argue that if you believe in the long-term trajectory of markets, then moments of discomfort can actually be the times when future returns are being quietly set up. In other words, while others are asking whether they should wait, he’s starting to think about where value might be emerging and whether this is a chance to invest at more attractive levels.

Colin isn’t necessarily being reckless or trying to perfectly time the bottom—but he is recognising that markets rarely offer opportunity when everything feels calm and certain.

He then points to the fact that some of the best days in the market tend to come very close to the worst ones. In fact, if you look back over time, a significant proportion of the strongest single-day gains have occurred within days or weeks of sharp declines.

Now this creates a challenge, because if you step out of the market during periods of uncertainty, you don’t just avoid the bad days—you risk missing the recovery as well. And missing even a small number of those strong rebound days can have a meaningful impact on long-term returns.

So from his point of view, the question isn’t whether volatility is uncomfortable—it always is—but whether stepping aside risks missing the very moments that drive long-term growth.

Eddie Economist, meanwhile, brings the conversation back to the fundamentals—precise, data-driven, and quietly confident in the numbers. He’s less interested in the headlines and more focused on the underlying mechanics—how energy prices feed into inflation, how inflation influences interest rates, and how those factors combine to affect economic growth. His argument is not emotional, but it does highlight where the real pressure points may lie.

Eddie Economist, meanwhile, brings the conversation back to the fundamentals—precise, data-driven, and quietly confident in the numbers. He’s less interested in the headlines and more focused on the underlying mechanics—how energy prices feed into inflation, how inflation influences interest rates, and how those factors combine to affect economic growth. His argument is not emotional, but it does highlight where the real pressure points may lie.

Sitting slightly more quietly is Brenda Behaviour—observant, thoughtful, and more interested in people than predictions. She tends to view things through a different lens altogether. Her focus isn’t really on the event itself, but on how people respond to it. And her observation, backed by years of evidence, is that the biggest damage to long-term outcomes rarely comes from the event—it comes from the decisions people make in reaction to it.

Sitting slightly more quietly is Brenda Behaviour—observant, thoughtful, and more interested in people than predictions. She tends to view things through a different lens altogether. Her focus isn’t really on the event itself, but on how people respond to it. And her observation, backed by years of evidence, is that the biggest damage to long-term outcomes rarely comes from the event—it comes from the decisions people make in reaction to it.

Then there’s Conrad Contrarian, who will usually lean back in his chair with a slight smile and make the slightly uncomfortable point that there is always something going on. There has never been a time when everything felt calm, predictable, and perfectly safe to invest, and waiting for that moment has historically been a losing strategy.

Then there’s Conrad Contrarian, who will usually lean back in his chair with a slight smile and make the slightly uncomfortable point that there is always something going on. There has never been a time when everything felt calm, predictable, and perfectly safe to invest, and waiting for that moment has historically been a losing strategy.

And finally, there’s Rachel Researcher. She’s methodical, quietly confident, and armed with data rather than opinion. She’s less interested in what people think might happen and far more interested in what has actually happened before, so instead of debating possibilities, she looks back at previous periods of geopolitical tension—whether that’s wars, oil shocks, or global crises.

And finally, there’s Rachel Researcher. She’s methodical, quietly confident, and armed with data rather than opinion. She’s less interested in what people think might happen and far more interested in what has actually happened before, so instead of debating possibilities, she looks back at previous periods of geopolitical tension—whether that’s wars, oil shocks, or global crises.

And what she finds is a pattern that repeats itself more often than you might expect.

Markets typically fall when uncertainty first appears, they become volatile as events unfold, but over time they recover and move on. In many cases, that recovery begins before the situation itself has fully resolved, as markets start to price in a future beyond the immediate crisis.

So her conclusion isn’t that risk doesn’t exist—it clearly does—but rather that reacting emotionally to that risk has historically been more damaging than the events themselves.

Out of interest…, before we move on, which of these characters do you most relate to? I have to admit, I’m more of a Gary Growth mixed with a portion of Rachel researcher….although I would probably enjoy conversations with Brenda behaviour due to my interest in financial psychology. Feel free to message mw with your thoughts on this if you want.

So… What Should You Actually Do?

OK, lets eave the meeting room now, come back into a quieter space, and start to think about what this actually means for you and your plan. Because the reality is that all of those perspectives have some truth to them, but none of them on their own give you a complete answer.

The natural instinct at times like this is to wait—to let things settle, to see how events unfold, and to invest when everything feels a little clearer. On the surface, that sounds entirely sensible but in practice, it rarely works as intended, because by the time things feel certain, markets have usually already adjusted, and what felt like caution can quietly turn into missed opportunity.

At the same time, committing everything immediately can feel uncomfortable, particularly when the backdrop feels unstable.

So the answer, in most cases, a sensible option may sit somewhere in the middle. As someone who is waiting to use my allowances my gut instinct is to be like Gary and put the maximum I can into the markets knowing that, for definite, I will be buying units cheaper than I would have been a month or more ago. However, Cautious Colin is having an impact at the moment and making me think it may be sensible to put 50% into the markets and then drip-feed the remainder in over the next 3 months (but definitely no longer than that).

Where Your Plan Comes In

For those of you that are clients, this is exactly why we build your financial plans the way we do. We don’t assume perfect conditions, smooth markets, or a calm global backdrop. Instead, we assume that disruption will happen, that volatility will appear from time to time, and that there will be periods where things feel uncertain.

Because there always are.

In practical terms, that means we deliberately build in a degree of conservatism into your lifetime cash flows. We might assume investment returns of around inflation plus 1.5%, while cash may be modelled at inflation minus 2.5%. We typically allow for you to live longer than average—often around 10% beyond standard life expectancy assumptions—and unless we’ve agreed otherwise, we assume you maintain your lifestyle throughout. All of this is designed to create resilience, so that when real-world uncertainty shows up, it doesn’t derail the plan—it’s already been accounted for.

Alongside those assumptions, we also anchor decisions around a few key measures within your plan—your capacity for loss, the level of investment return actually required to achieve your goals, and your future spending capacity.

These become the real drivers behind any recommendation, because they give context to decisions. They help answer questions like:

- can you afford to take more risk?

- do you actually need to and

- how much flexibility exists within your plan if markets don’t behave as expected?

Without that framework, it becomes much harder to make confident decisions. You’re left reacting to headlines, second-guessing timing, and trying to make complex financial choices without a clear reference point.

One of the advantages of having that level of clarity is that we can then actively stress-test your plan—often as part of our annual review meetings—by modelling different scenarios. We can look at what happens if inflation remains higher for longer, if markets are more volatile, or if growth is slower than expected.

And in most cases, what we see is not a plan that falls apart, but one that flexes and adjusts while still remaining on track.

With it, decisions become far more grounded, because they’re anchored in your plan rather than the noise around you.

A More Practical Way to Approach This

So, rather than asking whether now is the perfect time to invest, a more useful question is whether investing now aligns with your long-term plan. If it does, then short-term uncertainty becomes far less important.

That doesn’t mean you have to ignore how you feel about it, because comfort and confidence do matter. In many cases, a balanced approach works well investing a meaningful portion now to make use of allowances, while phasing the remainder over a short period if that helps you move forward with greater confidence.

Not because it’s mathematically perfect, but because it’s something you can stick with.

Final Thought

There will always be something going on, and there will always be reasons to wait. But waiting for certainty has never really been a strategy whilst having a plan that works, despite uncertainty, is.

So if you’re currently weighing up whether to invest, top up, or make use of the new tax year allowances, the answer is unlikely to come from the news. It will come from your plan—and your ability to stick to it.

Happy investing

Brian

PS As always, if you’d like to talk anything through or simply sense-check your thinking, I’m here.

No crystal ball, no guarantees—just a plan, and a steady hand when it matters.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}