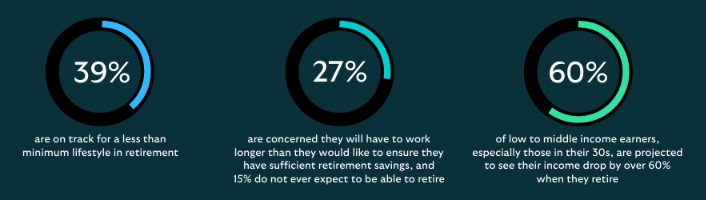

The headline figures from the latest Scottish Widows’ latest retirement report makes for uncomfortable reading. Roughly one in three UK workers, the research suggests, will not accumulate sufficient savings to fund even a basic standard of living in retirement. It is a sobering statistic — and rightly so. But here is where I want to take a slight detour from the conversation that usually follows.

Because the people I worry about most are not necessarily the ones that report was written about.

They are the successful solicitor in her late fifties who has dutifully contributed to her pension for three decades. The business owner who has built genuine wealth but has never quite sat down to join the dots. The senior executive approaching 60 with a healthy-looking SIPP, a decent property, some ISAs, and a growing unease he cannot quite articulate. They are, on paper, the people who have done everything right. And yet, in twenty-five years of retirement planning conversations, I have come to believe that financial success and retirement readiness are two very different things — and that the gap between them is both more common and more consequential than most people realise.

A Pension Pot Is Not a Retirement Plan

Let me say that again, because it bears repeating: a pension pot is not a retirement plan.

It is a starting point. An important one, certainly. But the moment we treat a large accumulated fund as the destination rather than a resource, we have already made a subtle but significant planning error.

The Scottish Widows report is fundamentally about people who will struggle to fill the tank. What concerns me — in an entirely different context — are the people who have filled the tank, started the engine, but have absolutely no map. They know they want to get somewhere comfortable. They have a reasonable sense they have enough fuel. But when you ask them to describe precisely where they are going, how long the journey will take, what it will cost along the way, and what happens if the road changes — the answers become rather vaguer than the balance on their pension statement would suggest.

Retirement planning is not about hitting a magic number. I see this misconception constantly. “If I can just get to a million pounds,” the thinking goes, “I’ll be fine.” Perhaps. But fine doing what, exactly? Fine for how long? Fine under what circumstances? Fine if inflation does what it has occasionally done in the past and erodes the purchasing power of that million rather more aggressively than the cautious cashflow model assumed?

The Risks That Successful People Don’t See Coming

There is a particular set of retirement planning blind spots that seem almost uniquely concentrated among the financially successful. I say this with genuine affection, not criticism — because in many ways, the habits that build wealth actively work against the mindset required to plan retirement well.

Longevity, for instance. Most of my clients intellectually understand that people are living longer. Far fewer have genuinely absorbed what that means in practice. A healthy couple aged 60 today faces a meaningful statistical probability that one of them will reach their late eighties or even their nineties. We are not talking about planning for a comfortable decade. We are talking about potentially funding thirty or thirty-five years of retirement — a period longer than many people’s entire working careers. The implications of that for how assets need to be structured, how income needs to be sustained, and how investments need to behave are profound. And yet the typical retirement conversation — even at a fairly sophisticated level — rarely extends much beyond the first ten or fifteen years in any meaningful way.

Then there is inflation. Not the dramatic headline variety that grabs the news, but the slow, grinding, entirely unremarkable inflation that simply happens across decades. Two percent a year sounds almost harmlessly small. Compound it over thirty years and the real-terms purchasing power of a fixed income falls by nearly half. If your retirement income plan relies heavily on level income — certain types of pension annuity, rental income that hasn’t been actively managed, interest on cash — then you may be quietly, incrementally becoming poorer every single year of your retirement without ever receiving a single piece of alarming correspondence about it.

Withdrawal rates deserve a conversation of their own. There is a widely circulated rule of thumb — the so-called “four percent rule” — that has done an enormous amount of damage in the hands of people who apply it without understanding its limitations, its assumptions, or the American equity market conditions under which it was derived. The rate at which you can sustainably draw down a portfolio depends on the sequence of returns you encounter in early retirement, your asset allocation, your flexibility to adjust spending, your time horizon, and a dozen other factors that make a single percentage rule little more than a blunt instrument. I have sat with clients who were entirely relaxed about their withdrawal strategy until we actually stress-tested it — at which point “entirely relaxed” became “rather less relaxed, and grateful we are having this conversation now rather than at sixty-eight.”

The Map You Have Never Drawn

Many people spend more time planning a two-week holiday than they do planning a retirement that may last thirty years.

That is not an exaggeration designed to shock. It is a quiet truth that I have observed repeatedly across years of client work. We research hotels, compare reviews, agonise over connecting flights and travel insurance. We give the holiday serious, focused attention. Retirement, somehow, gets added to an emotional to-do list marked “important but not urgent” — and stays there, year after year, until urgency arrives of its own accord.

The real question is whether your assets can reliably support the life you want for the rest of your life. And answering that question properly requires something most people have never done: sitting down and actually modelling it. Not vaguely gesturing at a pot and hoping for the best, but genuinely working through what your desired retirement lifestyle costs, what it will likely cost in fifteen years, how your income sources stack up against that, where the gaps are, and what levers you have available to pull if circumstances change.

Cashflow planning — proper, detailed, stress-tested lifetime cashflow modelling — is one of the most transformative things an experienced financial planner can do with a client. Not because it always reveals problems, though sometimes it does. But because it replaces vague anxiety with genuine clarity, and clarity, in my experience, is both underrated and extraordinarily valuable.

The Money Is Only Half the Story

I want to be careful not to make this sound purely like an exercise in spreadsheets and stress tests. Because the truth is that even a technically perfect retirement financial plan can leave someone profoundly unprepared for retirement itself.

The emotional and psychological dimensions of retirement are, in my view, consistently underestimated — and almost entirely absent from mainstream financial planning conversations. What happens to identity when a career ends? Many of my most accomplished clients have spent forty years being defined, at least in part, by what they do. The business they built, the profession they mastered, the role they inhabited. Retirement does not just change their financial circumstances. It changes the answer to the question: who am I?

The loss of structure is real. The erosion of social connection — which for many professionals comes almost entirely from the workplace — is real. The shift in relationship dynamics when two people suddenly find themselves together most of the day, with none of the pressure valves that working life quietly provided, is very real indeed. I have seen retirements that were financially superb and personally rather difficult, and I have come to believe that the money, however important, is only one dimension of a much larger picture.

Purpose matters. The way you will spend your time matters. The relationships you will invest in, the passions you will pursue, the contribution you will make — these are not soft afterthoughts to be addressed once the pension is sorted. They are central to whether retirement will actually be the experience you have been working toward, or a long, slightly directionless weekend from which Monday never quite arrives.

And there is one final challenge I see frequently, which does not get nearly enough airtime: the psychological difficulty of actually spending the money. Successful people, almost by definition, have spent decades in accumulation mode. Saving is a discipline they have mastered. The idea of deliberately drawing down assets — watching a hard-built pension fund reduce rather than grow — triggers a deep discomfort in many people that no spreadsheet alone can resolve. I have known clients who were technically free to retire comfortably at sixty, and still working at sixty-seven, not because they needed to, but because they could not quite make the psychological shift. The confidence to actually enjoy retirement is a legitimate planning outcome — and one worth working toward deliberately.

A More Complete Approach

This is precisely why I developed the Retirement Readiness Method™ — a more holistic framework for approaching retirement that brings the financial and the personal into the same conversation.

Because the real question was never simply “do I have enough?” It was always “am I truly ready?” — and those are not the same question at all.

The Retirement Readiness Scorecard™ is a practical starting point: a structured tool designed to help people identify, honestly and specifically, where the gaps in their retirement preparation actually lie. Not to generate anxiety, but to generate clarity. To replace the vague background hum of retirement unease — which affects far more successful, financially comfortable people than the statistics tend to capture — with a genuine, grounded picture of where you stand and what, if anything, needs attention.

If you are the kind of person who has worked hard, planned carefully, and built something meaningful — and you find yourself with a quiet, nagging uncertainty about whether all of that translates neatly into the retirement you actually want — then you are not alone, and you are asking exactly the right question.

The worst retirement outcomes I have ever seen did not happen to people who saved too little. They happened to people who never looked closely enough at what they were saving for, or who arrived at retirement without ever having truly prepared themselves for what it would ask of them.

Take the time to look. You have spent decades building the resources. It is worth spending a little serious time making sure they will take you where you actually want to go.

You can start your retire ready process here https://retire-ready.scoreapp.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}