Prophets, Profits, and the Crash That’s Always Coming

Brian Butcher 2026-06-05T15:40:51+01:00A client rang me recently. Invested his pension with me [...]

A client rang me recently. Invested his pension with me [...]

There’s a story I keep hearing. Different person, different pension [...]

I took some clients for a coffee the other day. [...]

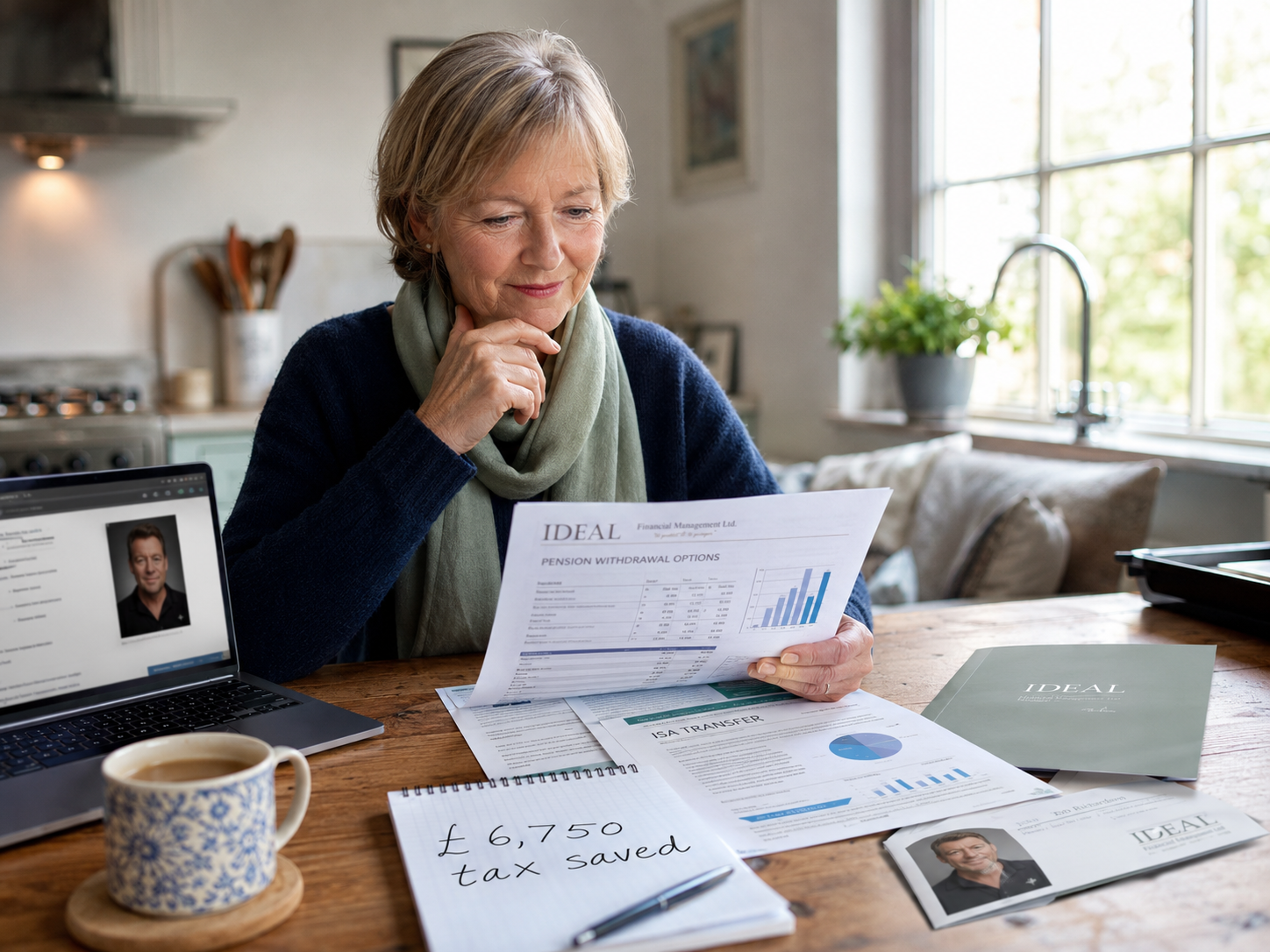

There's a quiet financial planning opportunity sitting unnoticed in thousands [...]

The headline figures from the latest Scottish Widows' latest retirement [...]

It’s that time again. A new tax year has quietly [...]

It’s happened. Financial Certainty Finally Guaranteed. After years of uncertainty, [...]

Over the past week, I’ve had several clients contact me [...]

When people begin thinking seriously about retirement planning, one of [...]

When it comes to money, we’d all like to believe [...]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}